🥕 Stock-based compensation: when do we worry?

I was recently reading through the annual report of Qualys, the cybersecurity company, and stumbled upon the following quote:

We understand that providing competitive compensation and benefits plays a critical role in attracting and retaining the best available personnel. That is why we offer robust compensation and benefits to our employees, including competitive base salaries, variable pay and equity awards.

This statement reflects the company's strong commitment to employee compensation, which they see as being an important factor in their long-term success.

Qualys's robust compensation is reflected in their financials. Currently stock-based compensation (SBC) represents 32.6% of their operating cash flow. But how much SBC is too much?

Stock-Based Compensation (SBC) and Its Impact on Financials

Ideally, when a company creates new shares, it should receive fresh capital in return, as seen in IPOs and secondary offerings. In the case of SBC, the issuance of new shares raises zero capital in return.

Unlike stock offerings, the result of SBC is share dilution, as the company's equity is now shared between more shareholders.

To prevent dilution, many companies (but not all) counteract SBC’s dilution effect by repurchasing stock from the secondary market, also known as buybacks. Share buybacks reduce the number of shares outstanding, which can help offset the dilution caused by SBC.

When a company issues stock-based compensation (SBC) and then performs a share buyback, the overall outcome is quite similar to a cash bonus — a reward given to employees.

Why Not Just Use Cash Bonuses Instead?

If the goal is simply to compensate employees, why not just give them a cash bonus instead of issuing stock? The main reason lies in the alignment of interests:

- Aligning Employees with Long-Term Performance: Rewarding employees with share ownership aligns their interests with the company’s long-term performance. Employees who own shares are motivated to drive the company’s growth, which benefits both them and shareholders.

- Flexibility in Resource Allocation: Stock-based compensation provides the company with more financial flexibility than cash bonuses. In contrast, cash bonuses reduce cash reserves, which may limit the company's ability to reinvest in growth opportunities.

So when should we worry about SBC?

If a company is counteracting SBC's dilution with buybacks, and they have adequate free cash flow to do so, then SBC isn't a concern.

It becomes a concern when:

- SBC is dilutionary

- SBC is a big part of free cash flow

- SBC is growing faster than FCF (suggesting it's not sustainable)

So how does Qualys measure up?

- Is SBC dilutionary? Over the last 5 years their share count has dropped by 10%, so clearly not.

- Is SBC a big part of FCF? Over the last 5 years, on average SBC represents 30.6% of FCF.

- Is SBC growing faster than FCF? They're pretty much neck-and-neck. FCF has grown at 20.7%, while SBC has grown at 20.0%.

So in conclusion, Qualys is counteracting the dilutionary impact of SBC and has adequate resources to do so.

So which companies should we be concerned about?

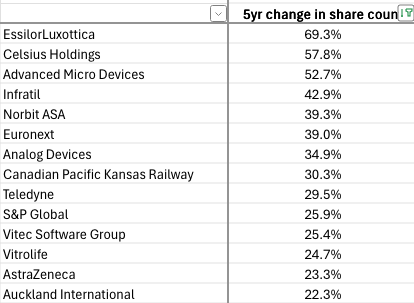

Let's start with the biggest dilutors. Here's a list of companies that have seen their share count go up by over 20% over the last 5 years.

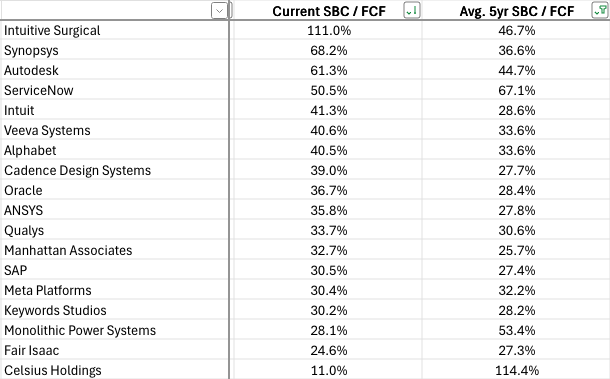

Now let's consider companies that have SBC as a large part of FCF. Here's a list of companies that all have high SBC compared to FCF, both currently and on average over the last 5 years.

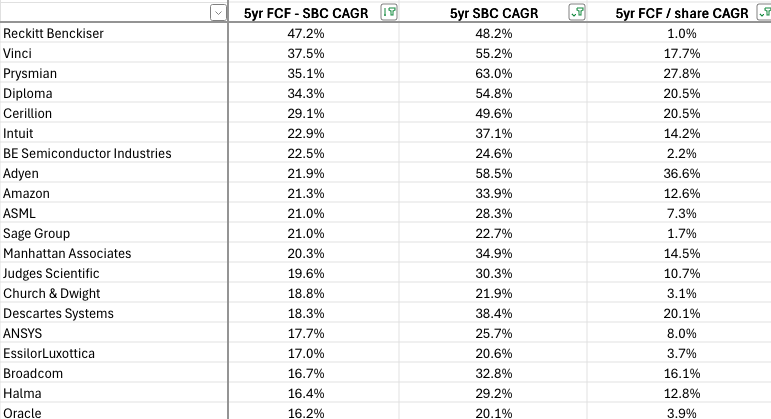

Finally, let's consider companies that have grown their SBC faster than their FCF. Here's a list of companies that have all grown their SBC faster than their FCF. Reckitt, for example, has grown its FCF by just 1% per year since 2019, but has grown SBC by 48.2% per year.

How does the Long Equity portfolio measure up?

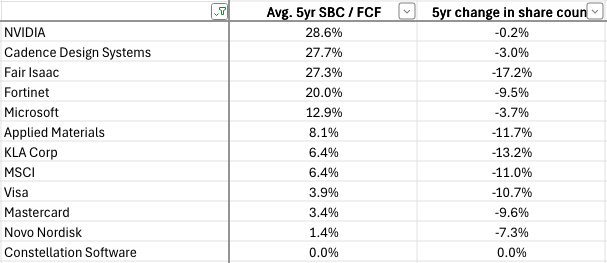

I currently have 12 stocks in my portfolio: Applied Materials, Cadence Design Systems, Constellation Software, Fair Isaac, Fortinet, KLA Corp, Mastercard, Microsoft, MSCI, NVIDIA, Novo Nordisk, and Visa.

The highest users of SBC are NVIDIA, Cadence, FICO and Fortinet. However, all have reduced their share count and have generated more than enough FCF to finance it.

In conclusion, SBC is not inherently problematic as long as it is managed and supported by strong cash flows. Investors should monitor SBC growth and dilution in companies to assess whether SBC is harmful and unsustainable. Companies that are overly reliant on SBC or experiencing excessive dilution could face challenges, but for those managing it well, SBC remains a valuable tool for aligning employees with long-term company performance.